This Illinois Appellate Court decision in divorce included a private business, two expert valuations, personal goodwill, and a marketability discount. My observations and commentary on key business valuation issues are below.

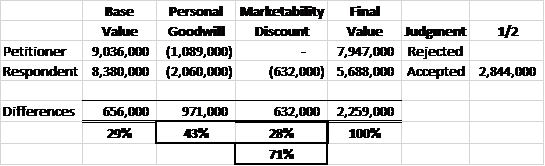

This is how the business valuation of “Littlestar” came out:

Goodwill – Enterprise & Personal

Observation:

The base valuations of the two experts differed relatively little. However, the respondent’s expert allocated nearly double what the petitioner’s expert allocated to personal goodwill.

Commentary:

The possibility of goodwill exists in nearly every private business valuation. Once goodwill is identified as an asset, the next step is to determine if goodwill contains both enterprise (marital) and personal (non-marital) components. Failing to identify and quantify personal goodwill will result in an incorrect business valuation in Illinois divorces.

Personal Goodwill Valuation Methods

Observation:

The petitioner’s expert used a “with-and-without” method to quantify personal goodwill. The respondent’s expert used the multi-attribute utility model (MUM) to quantify personal goodwill. The court accepted respondent expert’s MUM model.

Commentary:

An initial reaction might be to use MUM instead of “with-and-without” if you’re allocating personal goodwill in an Illinois divorce. Instead, the facts of a case should determine methodology. The key is to use judgement of qualitative factors and apply them to quantify goodwill. For example, personal goodwill factors could include:

- Expertise, skill, & reputation of individual.

- Personal abilities of the individual.

- Credentials, licenses, and experience of the individual.

- Customer confidence in the individual’s abilities.

- Personal relationships with customers maintained by an individual.

- Nature of services provided, i.e., personal.

- Individual’s direct impact on business profits.

The respondent testified one of Littlestar’s customers accounted for 83 percent of its business and 90 to 95 percent of the company’s profits. Assuming this was true, to the extent respondent’s personal relationship with this key customer was critical to maintaining Littlestar’s profitability, an expert might also allocate a large portion of total goodwill to personal goodwill. Stated differently, if the respondent left Littlestar without a non-compete agreement, would the key customer follow him? If so, a higher amount of personal goodwill would be justified. If not, it wouldn’t.

Lack of Marketability Discount

Observation:

The respondent’s expert applied a 10 percent lack of marketability discount which resulted in a $632,000 reduction in the value of the business.

Commentary:

A lack of marketability is used to quantify the inability of a seller of a private business to receive cash within a reasonable period after putting the business up for sale. Recent valuation literature has further split discussions of marketability into “lack of marketability” and “lack of liquidity” discounts. For example, a controlling interest in a private business might be marketable. However, it might not be immediately liquid or sellable quickly. Conversely, a small, non-controlling interest in the same private business may not be marketable or liquid. There is no direct empirical evidence to support a lack of marketability discount for a controlling interest. What was applied by the respondent’s expert was an estimation for “…working to sell smaller businesses, you have a broker involved” and there “would be a 10 percent cost to that to expedite that sale…” This is a liquidity discount, not a marketability discount. In addition, many valuation experts have argued that by applying a marketability or liquidity discount to a controlling interest, you’re valuing “net proceeds” or “net on a deal” as opposed to fair market value. By accepting a lack of marketability discount on a controlling interest, the court may have inadvertently valued Littlestar using a different standard of value other than Illinois’ precedent of fair market value.

Other Case Issues & Observations

- Business ruled marital property.

- Respondent’s expert had not divided goodwill before and prevailed.

- Equitable division of marital property and, specifically, the business.

- Respondent’s use of Littlestar “as his personal checking account”, purchase of Florida property for his girlfriend, and possible credibility problems.

- Petitioner’s contribution to the growth and success of Littlestar.

- Potential tax consequences to respondent ruled “hypothetical” since no order to convert Littlestar to cash, liquidate company, or pay petitioner over a seven-year period.

- Court dismissed respondent’s claim there was double-counting of personal goodwill – once in valuing Littlestar and once for maintenance – since personal goodwill was subtracted from valuation of Littlestar.

- Petitioner attacked petitioner’s own expert on valuation of Littlestar and, specifically, personal goodwill, and his lack of experience with it. Court disagreed.

- Petitioner’s expert “admitted that a lack of marketability discount is accepted in the valuation industry.” However, petitioner’s expert also stated, “he had never applied a lack of marketability discount to a controlling interest and that it was not appropriate in the present case where respondent held 100% of Littlestar.” My commentary: I concur with the petitioner’s expert on this point.

- Petitioner’s claim that court gave “substantial consideration” to respondent’s testimony on valuation of business without citing authority resulted in forfeiting consideration of the issue.

The link to the full case is here: https://bit.ly/2CSBqux and here: http://www.illinoiscourts.gov/R23_Orders/AppellateCourt/2018/2ndDistrict/2170656_R23.pdf

In re MARRIAGE OF VICKI L. PRESTON, Petitioner-Appellee and Cross-Appellant, and PHILIP E. PRESTON, Respondent-Appellant and Cross-Appellee. Appeal from the Circuit Court of Boone County. No. 13-D-79 Honorable John H. Young, Judge, Presiding.

Call me if you would like to discuss valuing a business in divorce or litigation.

Thanks,

Joshua L. Horn, CPA/ABV, CVA

Horn Valuation

Phone: 217-649-8794

Email: [email protected]

Website: hornvaluation.com

Curriculum Vitae: https://bit.ly/2ueQoq6

Attorney Tools: https://bit.ly/2QxmtEd

LinkedIn: http://bit.ly/2FsFqWJ

Twitter: https://bit.ly/2Ia3Mmj @hornvaluation

YouTube: http://bit.ly/2DlfXsj “horn valuation”

Facebook: https://bit.ly/2PO9c9d “horn valuation”

Horn Valuation is for attorneys & judges who believe there’s an easier way to settle business disputes and want to work with a valuation expert using fixed fees. I’ve been a CPA since 1999, a certified valuation analyst since 2008, and valued mom and pops to multi-million-dollar businesses. Call me today if you’re interested in working together on a valuation solution.